Cracking the Cycle: Shifting a Commodity Business to a Higher Earnings Floor

$1.15 billion in cash and zero debt, this industry leader just proved its structural transformation is real.

Intro

An off-the-beaten-path mid-cap at a $3.7 billion market capitalization, trading almost 40% below its 52-week high of $126.40. A long-term cyclical compounder and industry leader that benefits from market dominance and scale. This stock carries a fortress balance sheet with no debt, and close to a third of its total market capitalization in cash and equivalents. The board recently authorized a share repurchase program and consistently pays out one-third of net income, giving a current dividend yield of 6.16%. This company generally sees windfall profits during supply shocks and uses the cycle to take advantage of market share consolidation and opportunistic capital allocation.

Cal-Maine (CALM)

Mkt Cap: $3.7B

Current Price: $78.10 (6/12/26)

PE: 5.44

Div: 6.16%

52 Week High: $126.4 52 Week Low: $71.92

Company Description

Cal-Maine Foods, Inc., founded in 1957 and headquartered in Ridgeland, Mississippi, is the largest producer and distributor of fresh shell eggs in the United States. In fiscal 2025, the company sold approximately 1.3 billion dozen shell eggs, representing roughly 24% of total domestic shell egg consumption.

The company operates a fully integrated business model, meaning it controls almost the entire supply chain. Its operations include hatching chicks, growing and maintaining flocks of pullets, layers, and breeders, manufacturing its own feed, and producing, processing, packaging, and distributing the shell eggs.

Cal-Maine Foods’ product portfolio spans the full egg value ladder, categorized primarily into three areas:

• Conventional and Specialty Shell Eggs: The company produces standard conventional eggs alongside a rapidly growing portfolio of specialty eggs, which include cage-free, organic, brown, free-range, pasture-raised, and nutritionally enhanced options.

• Egg Products: This includes liquid and frozen egg products used primarily in the institutional, foodservice, and food manufacturing sectors.

• Prepared Foods: Expanding into value-added segments, the company offers ready-to-eat items such as hard-cooked eggs, pre-cooked egg patties, frozen omelets, specialty egg wraps, crepes, and protein pancakes.

The company markets its eggs under several well-known brands, including Egg-Land’s Best®, Land O’Lakes®, Farmhouse®, 4Grain®, Sunups®, Sunny Meadow®, MeadowCreek Foods®, and Crepini®.

Cal-Maine’s distribution network serves a diverse, blue-chip customer base across the majority of the U.S., including national and regional grocery store chains, club stores (such as Walmart and Sam’s Club), independent supermarkets, and foodservice distributors.

Ultimately, the company’s stated mission is to be the most sustainable producer and reliable supplier of consistent, high-quality fresh shell eggs, egg products, and prepared foods in the country, anchored by a “Culture of Sustainability” and operational excellence.

Why Now

The core thesis is not that the cycle has bottomed—I don’t know where the bottom is, and neither does anyone else. The thesis is that Cal-Maine is the company the egg cycle works for. Down-legs in this industry transfer share from leveraged, undercapitalized producers to the lowest-cost operator with the deepest pockets, and Cal-Maine has spent three decades consolidating 26 of them, mostly in moments like this one. It entered the current downswing with $1.15 billion in cash, zero debt, an active buyback, and a cage-free mandate about to force a capital reckoning on smaller rivals. If the down-leg runs longer and deeper than expected, Cal-Maine gets to buy more, cheaper. When supply eventually tightens—through flock economics or the next HPAI shock—the windfall accrues to whoever owns the capacity. The bet isn’t on the bottom; it’s on who owns the industry when the cycle turns. The dividend pays you to wait, and a newly possible takeout is optionality you aren’t paying for.

Management isn’t waiting out the cycle either. They view this downswing as an “important real-time test” of their structural shift toward specialty eggs and prepared foods—a mix that is actively reducing reliance on volatile spot markets and, in their words, positioning the business for “more durable normalized earnings power.” Q3 fiscal 2026 is the first data point: conventional prices down 70%, and the company still earned $1.06 diluted in the quarter—more than entire prior down-cycle years produced. One quarter doesn’t prove a transformation, but it’s evidence the test is being passed.

“Why Now” investment thesis:

1. A Historic Corporate Governance Overhaul (The “Discount” Removal). For its entire history as a public company, Cal-Maine traded at a potential valuation discount due to being a “controlled company” where the founding family held super-voting Class A shares. In April 2025, the family converted these shares into standard common stock and executed a secondary offering, causing their voting power to plummet from over 53% to approximately 6.1%. This event is a massive catalyst for institutional investors. It simplifies the capital structure, aligns voting rights with economic interests, and broadens the stock’s appeal to funds that strictly require single-class voting structures. Furthermore, without family control, the company is now fully exposed to potential activist investor campaigns or unsolicited acquisition offers, which could force further value-unlocking measures.

2. A Structural Pivot to Higher-Quality, Less Volatile Earnings. Management is actively redefining Cal-Maine so that it is no longer viewed as a “pure commodity business.” Through aggressive M&A, the company has acquired Echo Lake Foods and Creighton Brothers to rapidly build out a high-margin prepared foods and value-added egg products portfolio. As of the third quarter of fiscal 2026, specialty eggs and prepared foods combined accounted for a record 52.9% of total net sales, this may signal an important inflection point. To further insulate earnings, the company is shifting conventional egg sales toward “hybrid pricing models” that factor in the actual cost of production rather than relying entirely on volatile wholesale spot markets. This strategic pivot is designed to permanently raise the company’s earnings floor and reduce historical earnings volatility. In prior down-cycles, CALM printed $0.38 (FY20), $0.04 (FY21), and a loss (FY17). In Q3 fiscal 2026, with conventional egg prices down 70%, the company still earned $1.06 diluted in a single quarter. That’s the most direct evidence the transformation is real.

3. An Ideal Cyclical Entry Point Supported by Aggressive Capital Return. A ~$3.75 billion market cap, less $1.15 billion in cash, gives you an enterprise value around $2.6 billion for a business that just earned over $1.2 billion in a peak year and is structurally raising its trough. Commodity businesses are traditionally best bought at the bottom of their cycles. Cal-Maine is currently experiencing a severe cyclical contraction, with conventional egg prices crashing 70.1% in the third quarter of fiscal 2026 as the national layer flock recovered from HPAI outbreaks. However, unlike past down-cycles where the company simply suspended its variable dividend and waited for recovery, management is supporting the stock with a newly authorized $500 million share repurchase program. This provides a strong valuation floor while investors wait for the next upward swing in the commodity cycle. You don’t need to time the bottom because the balance sheet, buyback, and dividend pay you to wait while the next HPAI shock is a free call option you’re not paying for.

4. The Cage-Free Regulatory Moat. Ten U.S. states have passed legislation mandating cage-free egg sales, with deadlines ranging from 2022 to 2026, representing roughly 27% of the U.S. population. Transitioning to cage-free requires immense capital—estimated at $45 per bird, or roughly $6 billion industry-wide. With a fortress balance sheet and zero long-term debt, Cal-Maine has invested hundreds of millions of dollars to expand its cage-free capabilities organically and through acquisitions. Because smaller, undercapitalized competitors cannot afford this transition, Cal-Maine is perfectly positioned to capture outsized market share as these deadlines hit.

Growth

Cal-Maine Foods’ growth strategy is centered around three primary priorities: expanding specialty eggs and prepared foods, pursuing disciplined growth through acquisitions, and leveraging their scale, vertical integration, and financial strength. The company is actively executing a structural evolution to transition from a pure commodity shell-egg business into a more diversified, higher-value food company.

To achieve this, their strategy relies on:

• Disciplined M&A: Management targets acquisitions that provide geographic relevance, operating synergies, product portfolio expansion, and strong financial returns. Recent acquisitions have allowed them to enter new territories (like the Northeast and Mid-Atlantic via ISE America) and rapidly scale their prepared foods division (via Echo Lake Foods and Creighton Brothers).

• Organic Growth & Product Mix Shift: A core focus is expanding their cage-free, organic, pasture-raised, and free-range capacities to meet evolving consumer preferences and state-mandated animal welfare laws.

• Value-Added Products: They are expanding their reach in foodservice, retail, and institutional channels by growing their prepared foods portfolio, which includes hard-cooked eggs, pre-cooked egg patties, frozen omelets, and specialty egg wraps.

Total Addressable Market

Cal-Maine Foods addresses a massive consumer base, as shell eggs have an estimated U.S. household penetration rate of 96% to 98%. The underlying demand for this market is fundamentally driven by U.S. population growth, with Americans currently consuming an average of 271 to 292 eggs per person annually. Within this massive domestic market, Cal-Maine is the undisputed leader, recently capturing approximately 24% of all domestic shell egg consumption.

Management has actively grown the company’s total addressable market (TAM) through three primary avenues:

• Retail Network Expansion: Under the leadership of Chairman Adolphus B. Baker, Cal-Maine strategically expanded its total addressable market through joint ventures, partnerships, and franchise agreements. These enterprise synergies built an enhanced distribution network that now services more than 60,000 customer retail locations nationwide.

• Geographic Expansion: Historically concentrated in the Southwest, Southeast, Midwest, and Mid-Atlantic, the company has utilized recent acquisitions to unlock entirely new regional markets. For example, the acquisition of Fassio Egg Farms in Utah expanded their presence in the Western U.S., while the ISE America acquisition significantly enhanced their market reach into the Northeast by providing the company’s first production assets in Maryland, Delaware, and New Jersey.

• Category Expansion into Prepared Foods: By acquiring and investing in companies like Echo Lake Foods, MeadowCreek Foods, and Crepini, Cal-Maine is expanding its TAM beyond raw commodity shell eggs and into the large, growing, and highly stable value-added food category. Developing this portfolio of hard-cooked eggs, egg wraps, and frozen breakfast items allows the company to capture additional market share across commercial foodservice, quick-service restaurants, institutional, and industrial food product arenas.

Key Business Drivers

Wholesale Market Prices for Shell Eggs. The single most critical driver of Cal-Maine Foods’ top-line revenue is the wholesale market price of shell eggs. The company sells the majority of its conventional shell eggs based on formulas that take into account independently quoted regional wholesale market prices, such as those published by Urner Barry. Because conventional shell eggs are a commodity, small shifts in industry supply or consumer demand can cause extreme price volatility and cyclicality, which directly dictates the company’s profitability.

Feed Ingredient Costs. Feed costs represent the largest element of the company’s farm production costs, typically ranging from 53% to 63% of total farm production costs in recent years. The primary feed ingredients are corn and soybean meal. The prices of these commodities are highly volatile and are driven by uncontrollable external factors, including weather, crop yields, global supply and demand, transportation costs, and geopolitical instability (such as the Russia-Ukraine war and its impact on global grain exports). Increases in feed costs that are unaccompanied by corresponding increases in egg selling prices will severely compress the company’s margins.

Product Mix Shift (Specialty Eggs and Prepared Foods). To mitigate the extreme volatility of the commodity egg market, a major strategic growth driver is the expansion of value-added products, specifically specialty eggs and prepared foods.

• Specialty Eggs: Demand for specialty eggs (cage-free, organic, pasture-raised, free-range, and nutritionally enhanced) is rapidly growing. This shift is being driven by evolving consumer preferences, animal welfare legislation in multiple states, and pledges by major food retailers and restaurants to transition to exclusively cage-free supply chains. Specialty eggs are generally sold at negotiated prices tied to the cost of production rather than wholesale spot markets, which provides Cal-Maine with a higher, more stable earnings floor.

• Prepared Foods: The company is actively diversifying into the prepared foods segment through acquisitions like Echo Lake Foods and Creighton Brothers, as well as investments in MeadowCreek and Crepini. This allows Cal-Maine to leverage its shell egg production to manufacture higher-margin, ready-to-eat items like pre-cooked egg patties, frozen omelets, hard-cooked eggs, and egg wraps.

Biological Hazards and Avian Influenza (HPAI). Outbreaks of Highly Pathogenic Avian Influenza (HPAI) serve as a massive, dual-sided driver for the business. When HPAI strikes the national flock, it significantly restricts the domestic supply of laying hens, which historically drives wholesale egg prices—and Cal-Maine’s net income—to record highs. Conversely, HPAI poses a severe operational threat; outbreaks within Cal-Maine’s own facilities disrupt their supply chain, force the depopulation of affected flocks, and require millions of dollars to be spent on advanced biosecurity measures to prevent transmission.

Scale and Vertical Integration. Cal-Maine is the largest producer and distributor of fresh shell eggs in the U.S., recently supplying approximately 24% of domestic shell egg consumption. The company drives low-cost production through heavy vertical integration and modern “in-line” facilities, where eggs are mechanically gathered, cleaned, graded, and packaged directly at the location they are laid. Furthermore, to control quality and costs, Cal-Maine manufactures the vast majority of its own feed at mills located near its production plants.

Mergers and Acquisitions (M&A). Because the U.S. shell egg industry remains highly fragmented, disciplined M&A is a primary engine for growth. Management actively targets acquisitions to expand geographic reach, add immediate cage-free production capacity, and build out its prepared foods capabilities, having successfully integrated dozens of businesses since 1989.

Customer Concentration and Retail Leverage. The company relies heavily on a highly concentrated base of massive retail and club store customers. Cal-Maine’s top three customers typically account for nearly 50% of its total net sales, with Walmart (including Sam’s Club) alone representing roughly 29% to 34% of sales. This concentration gives massive consolidated retailers significant leverage to oppose price increases, demand specific promotional programs, or dictate supply chain requirements (like the shift to cage-free), making the retention of these blue-chip customers a vital driver of overall volume.

Management Outlook and Follow-Through

Management Outlook. Management’s outlook is highly focused on increasing the durability and predictability of the company’s earnings. By shifting their sales mix toward specialty eggs and prepared foods, they intend to create a higher earnings floor that is less susceptible to the wild cyclicality of the commodity egg market. Management notes that this is not just a pivot, but a disciplined evolution into a platform with multiple growth engines and improved long-term earnings visibility.

Management believes that general consumer demand for affordable, high-quality protein will continue to grow. To further stabilize revenues, they have begun shifting a higher proportion of their conventional egg sales to a “hybrid pricing model” that factors in their actual cost of production alongside wholesale market prices, which reduces profitability swings when egg prices are exceptionally high or low. Regarding input costs, management currently projects favorable stocks-to-use ratios for corn and soybeans, implying manageable feed prices in the near term, though they continuously monitor for volatility driven by weather and global supply chain uncertainties.

Management’s Track Record of Follow-Through. Management has a long, proven history of executing on its strategic promises and navigating extreme industry cycles (such as the devastating HPAI outbreaks):

• M&A Execution and Integration: Management has a time-tested framework for consolidation and has successfully identified, acquired, and integrated at least 26 companies since 1989. They have consistently followed through on their goal to acquire facilities near target markets to optimize their distribution network and reduce their reliance on outside egg purchases.

• Delivering on the Cage-Free Transition: When large retailers pledged to transition to cage-free eggs and various states passed minimum space requirements, management committed to scaling their infrastructure. They followed through by deploying hundreds of millions of dollars toward cage-free conversions and new builds, driving their specialty egg sales to account for over 50% of total shell egg sales in recent quarters.

• Expanding the Prepared Foods Portfolio: Management identified prepared and value-added foods as a key growth pillar to reduce earnings volatility and followed through with rapid, targeted investments. They invested in MeadowCreek Foods for hard-cooked eggs, formed a joint venture with Crepini for egg wraps and protein pancakes, and executed the major acquisitions of Echo Lake Foods and Creighton Brothers to anchor this new segment. As a result, specialty eggs and prepared foods combined recently accounted for over 52% of total net sales.

• Disciplined Capital Allocation: Management has strictly adhered to their variable dividend policy for decades, reliably paying out one-third of quarterly net income to shareholders during profitable periods. Furthermore, following through on their commitment to return excess capital to shareholders, they recently authorized and actively utilized a new $500 million share repurchase program.

Inside Ownership and Share Repurchases

For decades, the family kept their wealth highly concentrated in Cal-Maine Foods to maintain majority voting control and ensure stable, long-term governance, particularly following the death of the founder, Fred R. Adams, Jr., in 2020.

However, as the family members—specifically the founder’s four daughters and son-in-law Adolphus B. Baker—have shifted their focus toward individual estate planning and philanthropic endeavors, they recognized a need to generate liquidity and spread their personal financial risk across a broader mix of assets.

Converting their super-voting Class A shares into regular common stock and selling a significant portion of those shares (including the $50 million direct sale back to the company) allowed them to unlock the cash value of their highly concentrated holdings. Therefore, the loss of Cal-Maine’s “controlled company” status was not the result of a hostile takeover or a lack of confidence in the business, but rather a planned structural change to facilitate the insiders’ personal wealth diversification in an orderly manner.

The family still holds 2,791,854 shares of common stock that remain subject to registration rights for potential future sale. Under an ongoing Agreement Regarding Common Stock, if the family intends to sell any of these remaining shares, they must first offer the company a right of first refusal to purchase them. The purchase price for the company would reflect a 6% discount to the then-current 20-day volume-weighted average market price. If the company declines, the family may sell the shares in the open market subject to independent board approval.

Active Repurchase Program: The company may use its current $500 million share repurchase program to buy these shares directly from the family, provided any such transaction is approved by a Special Committee of independent directors. As of the most recent financial quarter ended February 28, 2026, the company had repurchased 1,175,867 shares in the open market under this program for $99.2 million, which, combined with the $50 million direct repurchase from the family in fiscal 2025, leaves $350.8 million still available.

Acquisitions and Acquisition Strategy

Cal-Maine Foods’ acquisitions are generally accretive, and the company maintains a growth strategy highly focused on “disciplined, accretive M&A.” Management explicitly targets acquisitions that provide operating synergies, enhance their product mix, improve their margin profile, and expand their geographic reach.

The company has a strong, time-tested track record of successful integrations, having acquired and integrated 26 businesses since 1989. Specific financial highlights from their recent acquisitions demonstrate this accretive focus:

• Echo Lake Foods (2025): The company expects this acquisition to be at least mid-single-digit accretive to earnings starting in fiscal 2026, while providing a return on equity in excess of the company’s cost of capital. It is also expected to offer an estimated $15 million annual synergy opportunity driven by egg purchasing efficiencies and SG&A savings.

• Mahard Egg Farm (2019): An investor presentation case study highlighted that by integrating the Mahard facilities and applying Cal-Maine’s management systems to resolve underperformance, the acquisition generated an estimated 260% return on investment (ROI), a 29% internal rate of return (IRR), and a rapid payback period of just 3.17 years.

Overall, Cal-Maine utilizes a strict investment framework to ensure their M&A activity not only builds scale and extends their reach into value-added categories, but also reduces overall earnings volatility and compounds long-term value for shareholders.

2018–2020: Strengthening the Core Foundation

• Featherland Egg Farms, Inc. (October 2018): Acquired commercial egg production and processing assets for $17.9 million, adding capacity for approximately 600,000 laying hens and a feed mill near Marion, Texas.

• Mahard Egg Farm (2019): Acquired assets relating to commercial shell egg production, processing, distribution, and sales to integrate into their South Central operations.

• Texas Egg Products, LLC (2020): Purchased the remaining non-controlling interests (having already held a 72.1% majority stake) to take 100% ownership of this egg products subsidiary.

2021: Expanding Specialty Capacity and Reach

• Red River Valley Egg Farm (May 2021): Acquired the remaining 50% membership interest from joint-venture partner Rose Acre Farms to take 100% ownership, adding approximately 1.7 million cage-free laying hens and pullet capacity in Texas.

• Southwest Specialty Eggs, LLC (December 2021): Made an additional strategic investment in this joint venture to acquire warehouse and distribution capabilities, expanding their specialty customer base across southern California, Arizona, and Nevada.

2023–2024: Geographic Expansion and Repurposing

• Fassio Egg Farms (2023): Acquired commercial shell egg facilities in Erda, Utah, adding a capacity of approximately 1.2 million primarily cage-free laying hens, alongside a feed mill and fertilizer production assets.

• Tyson Foods Facility (March 2024): Acquired a recently closed broiler processing plant, hatchery, and feed mill in Dexter, Missouri, to remodel and repurpose for shell egg and egg products production.

• ISE America, Inc. (June 2024): Acquired substantially all production and processing assets for approximately $110 million. This significantly enhanced market reach in the Northeast and Mid-Atlantic, adding laying hen capacity of 4.7 million (including 1.0 million cage-free) and providing Cal-Maine’s first production assets in Maryland, New Jersey, and Delaware.

Late 2024–2025: Advancing the Prepared Foods & Products Segment

• Crepini LLC (September 2024): Established a new joint venture by investing ~$6.75 million for a 51% controlling interest in Crepini Foods LLC. This accelerated the company’s expansion into prepared foods like egg wraps, protein pancakes, and crepes.

• MeadowCreek Foods (November 2024): Originally established as a joint venture in 2021 to anchor the hard-cooked egg segment, Cal-Maine Foods acquired the remaining 9.23% ownership interest in November 2024, converting it into a wholly owned subsidiary.

• Deal-Rite Feeds, Inc. (February 2025): Acquired two feed mills, storage facilities, and a retail feed sales business in North Carolina for approximately $4.7 million to support nearby shell egg production.

• Echo Lake Foods (June 2025): Acquired the ready-to-eat egg products and breakfast foods producer (waffles, pancakes, frozen omelets, etc.) for a purchase price of ~$230 million after tax benefits.

• Clean Egg, LLC (October 2025): Acquired production assets in Langwood, Texas, for approximately $23.7 million, adding 677,000 brown cage-free and free-range layers and pullets.

2026: Continued Value-Added Integration

• Creighton Brothers & Crystal Lake LLC (March 2026): Acquired shell egg, egg products, and prepared foods assets in Warsaw, Indiana, for approximately $128.5 million. This brought in 3.2 million laying hens (500,000 cage-free) and further integrated the supply chain for their growing prepared foods business.

Moat

Unmatched Scale and Market Dominance. Cal-Maine Foods possesses a massive scale advantage as the undisputed largest producer and distributor of fresh shell eggs in the United States. The company controls roughly 24% of domestic shell egg consumption. Managing a flock that has grown to nearly 50 million layers, Cal-Maine can reliably service the immense volume needs of the country’s largest blue-chip retailers, such as Walmart, H-E-B, and Publix, making them an indispensable supply chain partner.

The Low-Cost Moat: “In-Line” Operations. The core of Cal-Maine’s competitive moat is its highly efficient, vertically integrated operating model, which allows it to remain the low-cost supplier in its markets. Substantially all of the company’s farms feature modern “in-line” facilities. In these facilities, eggs are mechanically gathered, cleaned, graded, and packaged at the exact location where they are laid. This setup generates significant cost savings by eliminating the need to transport eggs to separate processing plants, reduces labor dependency, and yields a higher percentage of premium USDA Grade A eggs, which sell at higher market prices.

Vertical Integration of the Supply Chain. Cal-Maine controls almost every variable of its production. Their integrated operations include hatching chicks, growing and maintaining flocks, producing shell eggs, and distributing them. Crucially, because feed is the largest and most volatile cost component in egg production, Cal-Maine formulates and manufactures the vast majority of its own feed at mills located adjacent to its production plants. This self-sufficiency provides tight quality control over the hens’ diets and optimizes supply chain logistics.

Product Diversification and Premiumization. To defend against the extreme price volatility of conventional commodity eggs, Cal-Maine has aggressively expanded its moat into higher-margin, less volatile product categories.

• Specialty Eggs: They have invested hundreds of millions of dollars to expand cage-free, organic, pasture-raised, and free-range egg capacity to align with consumer trends and state-mandated animal welfare laws. Because these specialty eggs are often sold on negotiated cost-plus or long-term pricing frameworks rather than spot commodity markets, they provide a much more stable earnings floor.

• Prepared Foods: The company is rapidly transforming from a pure shell-egg producer into a diversified food company. Strategic acquisitions and joint ventures like Echo Lake Foods (waffles, pancakes, frozen omelets), MeadowCreek Foods (hard-cooked eggs), and Crepini (egg wraps) allow Cal-Maine to upcycle its own eggs into value-added, ready-to-eat products for retail and foodservice channels, further insulating the company from commodity swings.

Geographic Proximity and Distribution Efficiencies. Cal-Maine specifically targets M&A opportunities and facility expansions that keep its operations geographically close to its end customers. Shell eggs are highly perishable, and customer inventory typically requires short-term, rapid replenishment (often within 7 to 30 days). By maintaining an extensive, localized distribution network across the majority of the U.S., Cal-Maine can reduce freight costs, capture backhaul delivery efficiencies, and guarantee supply reliability that smaller regional competitors cannot match.

Financial Fortress. Finally, Cal-Maine’s moat is protected by a remarkably disciplined balance sheet. Operating with massive cash reserves and virtually zero debt, the company can comfortably weather periods of low egg prices or massive industry disruptions, such as the catastrophic Highly Pathogenic Avian Influenza (HPAI) outbreaks. This financial strength allows them to continually reinvest in automation, fund synergistic acquisitions during industry downturns, and consistently return capital to shareholders.

Competition

Key Competitors. Cal-Maine is the undisputed market leader, holding approximately 14% to 15% of the total U.S. layer hen flock. According to industry rankings, its closest top-tier competitors include:

• Rose Acre Farms (roughly 8% to 9% of the U.S. flock).

• Hillandale Farms (~6% of the U.S. flock).

• Versova Holdings (~6% of the U.S. flock).

• Daybreak Foods (~4% to 6% of the U.S. flock).

A New Competitive Front: Prepared Foods. As Cal-Maine has aggressively expanded its growth strategy into the prepared and value-added foods sector—most notably through its acquisition of Echo Lake Foods and strategic investments in Crepini and MeadowCreek—the company faces an entirely new set of competitive pressures. In the prepared foods market, Cal-Maine competes against established prepared food companies, restaurants, grocery stores, and convenience stores. Management acknowledges that many of these competitors have significantly more experience operating prepared and convenience foods businesses than Cal-Maine does.

Customer Leverage and Consolidation. Compounding these competitive pressures is the ongoing consolidation of Cal-Maine’s customer base. Supermarkets, warehouse clubs, and food distributors are merging, which produces massive buyers (like Walmart, their largest customer) with immense buying power. These consolidated customers are highly capable of operating with reduced inventories, opposing price increases, demanding lower pricing, and requiring specifically tailored products and promotional programs.

Risks to Business

Market Volatility and Commodity Exposure

• Egg Price Cyclicality: Shell eggs are pure commodities, and their wholesale prices are highly volatile and cyclical. Because demand is relatively steady and price-inelastic, small increases in industry production (oversupply) or decreases in demand can cause dramatic drops in egg prices, directly compressing the company’s revenues and profits.

• Feed Cost Fluctuations: Feed ingredients—primarily corn and soybean meal—are Cal-Maine’s largest farm production expense, historically representing 53% to 63% of these costs. The company has virtually no control over these prices, which are impacted by weather, global supply and demand, transportation costs, and geopolitical instability (such as the Russia-Ukraine war). If feed costs rise but egg prices do not, margins are severely squeezed.

Biological and Agricultural Hazards

• Highly Pathogenic Avian Influenza (HPAI): HPAI is a persistent and devastating operational threat. Outbreaks within Cal-Maine’s own facilities—such as those experienced in Kansas, Texas, and Maryland between 2024 and 2026—force the immediate depopulation of millions of laying hens and pullets, severely disrupting supply capabilities.

• Extreme Weather and Climate Change: Operations are vulnerable to natural disasters like droughts, floods, hurricanes, and extreme temperatures. High heat and humidity cause stress on poultry, while erratic weather can destroy local feed crops, leading to significantly higher input costs or facility damage.

Customer Concentration and Retailer Leverage

• Heavy Reliance on Top Customers: Cal-Maine’s top three customers generally account for roughly 45% to 51% of net sales, with Walmart (including Sam’s Club) alone representing roughly 29% to 34% of total sales.

• Pricing Pressure: The consolidation of supermarkets gives these massive buyers immense leverage to demand lower pricing, push back on price increases, and demand specific promotional programs. The loss of a major customer, or capitulating to aggressive pricing demands, would have a material adverse effect on financial results.

The Cage-Free Transition and Regulatory Pressures

• Capital Demands and Forecasting Risk: State mandates (like California’s Proposition 12) and retailer pledges require a massive industry-wide transition to cage-free eggs. Producing cage-free eggs requires significant capital expenditures and carries higher ongoing operating costs.

• Mismatched Supply and Demand: Because customers generally do not commit to long-term purchasing contracts, Cal-Maine faces the risk of over-estimating demand for expensive cage-free eggs (leading to an oversupply and poor return on investment) or under-estimating it (losing market share to competitors who lock up supply).

Food Safety and Contamination

• Microbial Contamination: Shell eggs and egg products are vulnerable to contamination by pathogens like Salmonella and Listeria. Even inadvertent shipments of contaminated or spoiled products could lead to product recalls, product liability claims, intense regulatory scrutiny, and a devastating loss of consumer confidence.

Acquisition Execution and Prepared Foods Expansion

• Integration Challenges: Cal-Maine’s growth strategy relies heavily on acquisitions (like Echo Lake Foods). Integrating these businesses may be more costly or time-consuming than expected, and the company may fail to realize anticipated synergies or financial returns.

• Lack of Experience in New Verticals: As Cal-Maine expands into value-added prepared foods, it faces intense competition from established food companies, restaurants, and grocery stores. Management acknowledges their experience in managing prepared foods is much more limited than in their traditional shell egg business.

Macroeconomic and Labor Constraints

• Labor Shortages and Wage Inflation: Operating remote farms requires a significant workforce. Decreased labor participation and competition for workers have forced the company to use more expensive contract labor and increase wages to attract and retain staff.

• Inflationary Pressures: Rising costs for packaging materials, transportation, fuel, and construction directly drag on profitability if they cannot be passed on to the consumer.

Legal and Governance Risks

• Litigation and Government Investigations: The company is subject to unpredictable legal proceedings, including DOJ civil investigative demands regarding antitrust conduct, state-level price-gouging claims, and massive antitrust lawsuits (like the Egg Products Plaintiffs case, which resulted in a $43.6 million treble damages judgment being appealed).

• Loss of “Controlled Company” Status: Following the founding family’s stock conversion and sell-down in 2025, Cal-Maine is no longer a “controlled company.” This exposes the business to an increased risk of unsolicited acquisitions, activist campaigns, or disruptions seeking to force changes in management or corporate governance.

Important Financial Metrics

The company explicitly identifies four key financial and non-financial performance measures as the most important metrics used to link executive compensation to overall company performance:

• Net income per dozen produced: A non-GAAP financial measure calculated by dividing the company’s net income by the total dozens of eggs produced.

• Dozens sold and produced: Absolute volume metrics that drive the company’s scale, market share, and revenue.

• Production cost per dozen: A critical efficiency measure, as farm production costs are the primary driver of the company’s overall cost of sales.

• Food quality and safety: A foundational non-financial metric that management believes ensures reliable and continued financial performance.

Beyond these executive compensation metrics, management consistently highlights several other key variables that dictate their financial results:

• Feed costs (per dozen produced): Feed ingredients (primarily corn and soybean meal) are the largest and most volatile component of farm production costs. Management measures feed cost on a per-dozen basis to track efficiency and margin impacts.

• Net average selling price per dozen: The wholesale market price for eggs dictates top-line revenue, and management tracks this closely across both conventional and specialty egg categories.

• Gross profit and operating margins: Because shell eggs are a highly cyclical commodity, the company evaluates gross profit and operating income as a percentage of net sales to measure profitability through extreme market cycles.

• Outside egg purchases (average cost per dozen): The cost and volume of eggs purchased from outside producers, which are used to supplement the company’s own flock production and fulfill customer orders.

Financial Analysis

Capital Allocation and Strategies

Cal-Maine Foods employs a highly disciplined capital allocation strategy designed to balance consistent shareholder returns with strategic reinvestment in the business, all while maintaining a fortress balance sheet to navigate the severe cyclicality of the shell egg industry.

Their capital allocation priorities are anchored by the following pillars:

1. Variable Dividend Policy. For decades, Cal-Maine has adhered to a strict variable dividend policy, distributing one-third (33.3%) of its quarterly net income to shareholders. This policy directly ties shareholder returns to company performance. If the company records a net loss in a quarter, it suspends dividend payments until it returns to profitability on a cumulative basis. These dividend payments are subject to restrictions under the company’s credit facility, requiring them to maintain at least $50 million in combined cash and credit availability to issue a payout.

2. Share Repurchase Program. To expand its options for returning capital to shareholders, the Board approved a $500 million share repurchase program in February 2025. Management actively uses this program to opportunistically buy back stock in the open market and through privately negotiated transactions. Additionally, as part of the founding family’s portfolio diversification efforts, the company may use this program to repurchase shares directly from the family, subject to independent board approval.

3. Organic Growth and Cage-Free Capital Expenditures. A massive portion of Cal-Maine’s free cash flow is continually deployed toward organic growth, with a primary focus on expanding cage-free and specialty egg production capacity. Because major retailers and state mandates are pushing the industry toward cage-free environments, management has invested hundreds of millions of dollars to construct new facilities and convert existing conventional housing. Capital is also actively allocated to modernize infrastructure, enhance biosecurity against avian influenza (HPAI), and expand value-added processing and prepared foods capabilities.

4. Disciplined Mergers & Acquisitions (M&A). Cal-Maine leverages its strong liquidity to execute disciplined, accretive M&A. Management evaluates acquisition targets based on strict criteria, including geographic relevance, operating synergies, proximity to customers, and strong financial returns. Recent strategic acquisitions, such as Echo Lake Foods, ISE America, and Creighton Brothers, demonstrate their strategy to deploy capital to build scale, increase cage-free capacity, and aggressively expand into the higher-margin prepared foods sector.

5. Balance Sheet and Liquidity Optimization. Underpinning all of these allocations is a commitment to a debt-free financial fortress. The company traditionally operates with zero long-term debt and maintains massive pools of cash, cash equivalents, and short-term available-for-sale investment securities to fund operations and acquisitions during cyclical market downturns. To provide additional financial flexibility for future growth, the company also maintains a $250 million senior secured revolving credit facility, which generally remains completely undrawn.

Revenue Breakdown

While Cal-Maine Foods operates as a fully integrated company with a single reporting segment, they disaggregate their revenue across two main dimensions: by product category and by sales channel.

To give you a complete picture, here is the revenue breakdown for their most recently completed full fiscal year (fiscal 2025, ended May 31, 2025), as well as the latest year-to-date data reflecting their recent M&A expansion.

Fiscal Year 2025 Revenue Breakdown

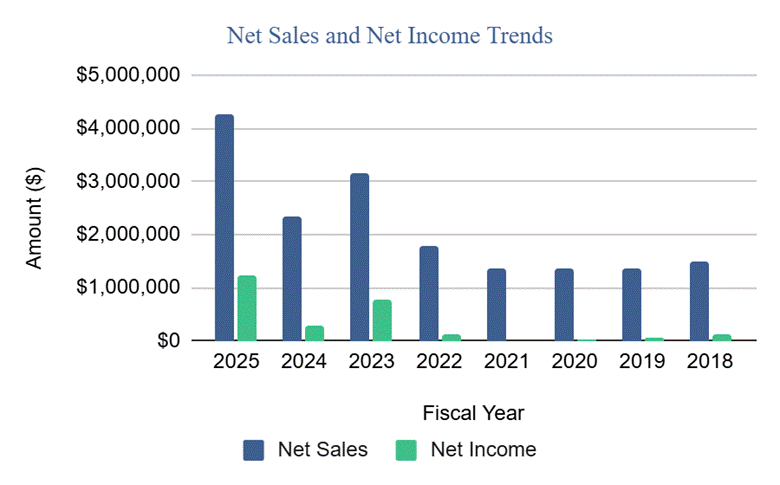

In fiscal 2025, the company generated a record $4.26 billion in total net sales.

By Product Category:

• Conventional Shell Eggs: $2.84 billion (66.5% of sales). These represent standard white shell eggs sold under private labels or brands like Sunups® and Sunny Meadow®.

• Specialty Shell Eggs: $1.18 billion (27.8% of sales). This higher-margin category includes cage-free, organic, pasture-raised, free-range, and nutritionally enhanced eggs sold under brands like Egg-Land’s Best® and Farmhouse®.

• Egg Products & Prepared Foods: $198.8 million (4.7% of sales). This includes liquid/frozen egg products for institutional use, as well as hard-cooked eggs.

• Other: $43.1 million (1.0% of sales). This consists of feed sales, miscellaneous byproducts, and resale products.

By Sales Channel:

• Retail: $3.61 billion (84.8% of sales). This channel includes national/regional grocery chains and club stores. Note: Customer concentration is very high here; Walmart (including Sam’s Club) alone accounted for 33.6% of the company’s total net sales in fiscal 2025.

• Foodservice: $608.2 million (14.3% of sales). Sales to distributors that supply restaurants, healthcare facilities, hotels, and education facilities.

• Other: $39.9 million (0.9% of sales).

Latest Year-To-Date Trends (First Three Quarters of Fiscal 2026)

The company’s revenue mix is actively shifting as a direct result of their recent M&A strategy (such as acquiring Echo Lake Foods and Crepini) and the nationwide push toward cage-free eggs. For the 39 weeks ended February 28, 2026, Cal-Maine generated $2.36 billion in net sales.

The breakdown for this most recent nine-month period highlights a massive shift in their product mix:

• Conventional Shell Eggs: $1.15 billion (48.7% of net sales)

• Specialty Shell Eggs: $858.3 million (36.4% of net sales)

• Prepared Foods: $219.2 million (up 604% year-over-year and 9.29% of net sales)

• Egg Products: $90.0 million

• Other: $38.6 million

Key Insight on the Revenue Mix Shift: Management’s strategy to move away from volatile commodity markets is succeeding. In the most recent standalone quarter (Q3 fiscal 2026), specialty shell egg sales actually surpassed conventional shell egg sales ($289.1 million vs. $283.2 million). Additionally, combined sales from specialty eggs and the newly supercharged prepared foods segment accounted for 52.9% of all net sales in Q3 fiscal 2026.

Revenue Volatility and Cyclicality

Because shell eggs are a commodity, Cal-Maine Foods’ revenue fluctuates dramatically based on the national egg supply, consumer demand, and resulting market prices.

Here is the total net sales breakdown over the full fiscal years 2018 to 2025:

• Fiscal 2018: $1.50 billion

• Fiscal 2019: $1.36 billion

• Fiscal 2020: $1.35 billion

• Fiscal 2021: $1.35 billion

• Fiscal 2022: $1.78 billion

• Fiscal 2023: $3.15 billion

• Fiscal 2024: $2.33 billion

• Fiscal 2025: $4.26 billion

The massive sales spikes in fiscal 2023 and 2025 were not the result of steady, organic volume growth, but rather historic supply disruptions. Severe outbreaks of Highly Pathogenic Avian Influenza (HPAI) forced the depopulation of tens of millions of commercial laying hens nationwide, creating a severe supply shortage that drove conventional egg selling prices to record highs.

Conversely, when the national egg supply recovers from these outbreaks, market prices crash, leading to steep revenue declines despite steady or growing sales volumes. For example, in fiscal 2024, sales dropped by roughly $800 million as the industry recovered from the 2022 HPAI outbreaks.

This downward trend is repeating in the current year. For the first three quarters of fiscal 2026, net sales dropped 25.3% to $2.36 billion, compared to $3.16 billion in the same period of fiscal 2025. This massive decline occurred because the U.S. egg supply improved and wholesale prices dropped significantly.

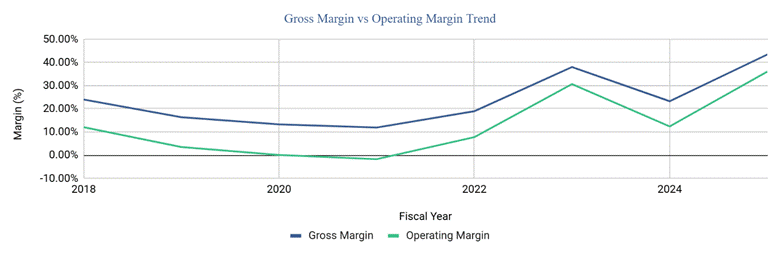

Gross profit and operating profit margins:

EPS

Cal-Maine Foods’ earnings per share (EPS) is highly cyclical, fluctuating dramatically based on the commodity prices of shell eggs, feed costs, and severe supply disruptions like Highly Pathogenic Avian Influenza (HPAI).

Here is the historical breakdown of the company’s basic and diluted EPS over the reported time periods:

Full Fiscal Years (2017–2025):

• Fiscal 2017: Basic $(1.54) | Diluted $(1.54) (net loss)

• Fiscal 2018: Basic $2.60 | Diluted $2.60

• Fiscal 2019: Basic $1.12 | Diluted $1.12

• Fiscal 2020: Basic $0.38 | Diluted $0.38

• Fiscal 2021: Basic $0.04 | Diluted $0.04

• Fiscal 2022: Basic $2.73 | Diluted $2.72

• Fiscal 2023: Basic $15.58 | Diluted $15.52

• Fiscal 2024: Basic $5.70 | Diluted $5.69

• Fiscal 2025: Basic $25.04 | Diluted $24.95

Latest Year-To-Date (Fiscal 2026):

• First Three Quarters of Fiscal 2026 (39 weeks ended February 28, 2026): Basic $7.37 | Diluted $7.34 (for the standalone Q3 fiscal 2026, EPS was Basic $1.07 | Diluted $1.06).

Key Takeaways on EPS Volatility: The EPS history clearly illustrates the extreme cyclicality of Cal-Maine’s business.

• The Lows: In years where the national egg supply was high or feed costs spiked without matching egg prices (such as 2017, 2020, and 2021), EPS remained suppressed or fell into a net loss.

• The Highs: Conversely, the massive EPS spikes in fiscal 2023 ($15.52 diluted) and fiscal 2025 ($24.95 diluted) were driven by devastating national outbreaks of HPAI. These outbreaks forced the depopulation of millions of laying hens across the country, heavily constraining the national egg supply and driving wholesale market prices to unprecedented record highs. When the industry begins to recover from these outbreaks and supply normalizes, market prices and Cal-Maine’s EPS typically contract (as seen in the drop from 2023 to 2024, and the current moderating trend in 2026).

Cost of Products Sold (Inventory and Supply Chain)

Cal-Maine Foods reports its inventory, supply chain, and production costs under “Cost of Sales.” Because shell eggs are a highly cyclical commodity, the company’s cost of products sold fluctuates significantly from year to year based on external factors like feed ingredient prices, labor and packaging inflation, and emergency outside egg purchases during supply shortages.

Here is the historical progression of Cal-Maine’s total cost of sales over the reported fiscal years:

• Fiscal 2018: $1.14 billion

• Fiscal 2019: $1.14 billion

• Fiscal 2020: $1.17 billion

• Fiscal 2021: $1.19 billion

• Fiscal 2022: $1.44 billion

• Fiscal 2023: $1.95 billion

• Fiscal 2024: $1.78 billion

• Fiscal 2025: $2.41 billion

• First Three Quarters of Fiscal 2026: $1.72 billion

Key Components and Drivers of Cost of Sales

To understand why costs escalated so dramatically—particularly peaking in fiscal 2025 at $2.41 billion—it helps to look at the primary sub-categories that make up these expenses:

Farm Production (The Feed Cost Driver). Farm production is typically the largest segment of the company’s costs. This encompasses the cost of growing and maintaining flocks, facility labor, flock amortization, and feed.

• Feed Costs: Feed ingredients (primarily corn and soybean meal) are highly volatile and generally account for 53% to 63% of farm production costs. Throughout fiscal 2022 and 2023, feed costs surged due to weather-related crop shortfalls, supply chain disruptions, and global instability from the Russia-Ukraine war impacting grain exports. Feed costs per dozen produced increased from $0.446 in 2021 to $0.676 in 2023. As grain prices moderated in 2024 and 2025, feed costs dropped back down to $0.490 per dozen in 2025.

Outside Egg Purchases (The HPAI Driver). When Cal-Maine cannot produce enough eggs to meet customer demand—often due to flock depopulations from Highly Pathogenic Avian Influenza (HPAI)—they are forced to buy eggs from outside producers on the open market.

• Because wholesale egg prices skyrocket during HPAI outbreaks, Cal-Maine has to buy these outside eggs at premium prices.

• In a normal year like 2021, outside egg purchases cost the company $177.6 million.

• During the massive HPAI outbreaks of fiscal 2023, this cost more than doubled to $379.8 million.

• During the resurgence of HPAI in fiscal 2025, outside egg purchases skyrocketed to a staggering $819.6 million, becoming a massive drag on the cost of sales.

Processing, Packaging, and Warehouse. This category tracks the costs of getting the eggs cleaned, graded, packaged, and stored.

• These costs steadily climbed from $222.8 million in 2019 to $396.1 million in 2025.

• The increases were primarily driven by systemic inflation, pandemic-era supply chain constraints on packaging materials, manufacturer surcharges, and consistent wage increases implemented to combat severe labor shortages.

Egg Products and Prepared Foods. Historically a small portion of their costs ($29.0 million in 2019), this category has expanded rapidly as part of management’s strategic shift toward value-added products. Following the recent acquisitions of Echo Lake Foods and Creighton Brothers, the cost of sales for egg products and prepared foods jumped to $159.6 million in fiscal 2025 and has already reached $179.9 million for prepared foods plus $70.1 million for egg products in just the first three quarters of fiscal 2026.

Operating Expenses (Selling and Administrative)

Cal-Maine Foods reports its operating expenses under the line item selling, general, and administrative (SG&A) expenses. As a percentage of net sales, SG&A historically fluctuates between roughly 7% and 14%, depending largely on the extreme cyclicality of the company’s top-line revenue. SG&A expenses have grown alongside the company’s recent expansion, rising from $252.6 million in fiscal 2024 to $314.4 million in fiscal 2025.

Assets

As of the company’s most recent financial reporting period ended February 28, 2026, Cal-Maine Foods has total assets of $3.14 billion.

The company’s biggest asset categories are:

• Property, Plant, and Equipment (PP&E), net: Valued at $1.22 billion, this is the company’s single largest asset category. This massive carrying value reflects the company’s vertically integrated, capital-intensive physical footprint. It encompasses their owned land (over 33,000 acres), feed mills, breeding facilities, hatcheries, processing and packaging plants, and their extensive layer and pullet housing, including hundreds of millions of dollars invested in new cage-free facilities.

• Cash and Short-Term Investments: Combined, these liquid assets represent $1.15 billion. This fortress balance sheet is made up of $392.2 million in cash and cash equivalents alongside $759.8 million in available-for-sale investment securities. This deep liquidity pool enables their debt-free balance sheet, funds their aggressive M&A pipeline, and supports their variable dividend policy.

• Inventories: Valued at $348.9 million. The most valuable component of their inventory is actually their live birds; the flock (net of amortization) is valued at $176.3 million. This is followed by feed and supplies at $114.0 million, and raw materials and finished egg products at $58.7 million.

• Receivables, net: Valued at $234.9 million. This includes trade receivables from their grocery and foodservice customers, as well as income tax receivables.

Debt

Cal-Maine Foods operates with a highly conservative balance sheet, consistently reporting zero long-term debt outstanding in recent fiscal years. To provide financial flexibility and support its growth, the company maintains a $250 million senior secured revolving credit facility, which was amended and restated in November 2021 with a five-year term. The company generally keeps this facility entirely undrawn, utilizing it only to issue a small amount of standby letters of credit (typically around $4.1 million to $4.7 million) for the benefit of certain insurance companies. Borrowings under this agreement are subject to customary financial covenants, primarily requiring the company to maintain a maximum total funded debt to capitalization ratio of no greater than 50% and a minimum tangible net worth of $700 million plus 50% of positive net income less permitted restricted payments.

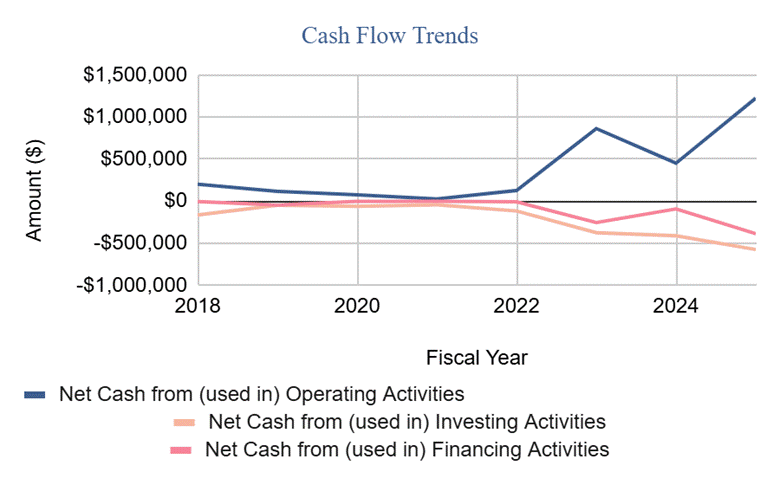

Operating Cash Flows and Seasonal Drivers

The company’s operating cash flows are highly volatile and are primarily dictated by the spread between wholesale shell egg prices and feed ingredient costs (primarily corn and soybean meal). Beyond commodity market cyclicality, operating cash flows are heavily influenced by predictable seasonal drivers. Retail sales and prices for shell eggs are historically highest during the fall and winter months, driven by the start of the school year and major holiday baking seasons around Thanksgiving, Christmas, and Easter.

Conversely, a natural increase in flock production in the spring and early summer typically leads to an oversupply and depresses prices, making the summer months the weakest period for sales. Consequently, Cal-Maine generally experiences lower net income and operating cash flows in its first and fourth fiscal quarters (ending in August/September and May/June, respectively), which is when the company’s need for working capital is at its highest.

Investing and Financing Cash Flows

Cal-Maine’s investing cash flows are heavily directed toward capital expenditures, strategic acquisitions, and the management of its massive short-term investment portfolio. The company routinely deploys hundreds of millions of dollars toward organic growth, specifically focusing on building and converting facilities to expand its cage-free production capacity to meet evolving retail mandates. In recent years, investing cash outflows have also been driven by an aggressive acquisition strategy, including the purchases of Fassio Egg Farms, ISE America, Clean Egg, and Echo Lake Foods.

On the financing side, cash flows are largely dominated by the company’s long-standing variable dividend policy, which mandates returning one-third of quarterly net income to shareholders during profitable periods. Furthermore, financing cash outflows have recently expanded to include significant share repurchases following the Board of Directors’ authorization of a new $500 million share repurchase program in early 2025.

What I Am Watching Going Forward

Bird Flu and the Cyclical Downswing. The primary driver of the current cycle downswing is the recovery of the national egg supply following severe Highly Pathogenic Avian Influenza (HPAI) disruptions. During the third quarter of fiscal 2026, the USDA reported a 70.6% year-over-year reduction in hen depopulations. As a result, the average national layer flock grew by 2.2% to reach 310.8 million hens.

Customer Concentration and Walmart. Cal-Maine Foods has historically operated with a highly concentrated customer base, relying heavily on a select group of national and regional retailers. Walmart Inc. (including Sam’s Club) is by far their largest individual customer, consistently representing roughly 34% of the company’s total net sales in recent years. For context, over the last three completed fiscal years, Walmart alone accounted for 34.2% of net sales in fiscal 2023, 34.0% in fiscal 2024, and 33.6% in fiscal 2025. Because the top three customers collectively make up around half of the company’s entire revenue (49.2% in fiscal 2025), management notes that a loss of Walmart or any other major retailer—or a substantial reduction in their purchase volumes or pricing—would have a material adverse effect on Cal-Maine’s overall business and financial results.

Execution of the Prepared Foods Pivot. Cal-Maine is actively trying to break away from its “pure commodity” label by aggressively acquiring value-added and prepared food companies, such as the $258 million (gross) acquisition of Echo Lake Foods, the Crepini joint venture, and MeadowCreek.

• Can management successfully integrate these distinct businesses? Management has acknowledged that their experience in operating prepared and convenience food businesses is much more limited than their historic shell egg operations. What operational challenges or cost overruns are they facing in integrating Echo Lake Foods?

• Will prepared foods truly insulate earnings? Will the higher margins of protein pancakes, egg wraps, and hard-cooked eggs be enough to meaningfully offset the massive volatility of the raw shell egg commodity cycle?

Legal, Regulatory, and Antitrust Exposure. The company is facing severe legal and government scrutiny regarding its pricing and supply practices.

• What is the ultimate exposure to the DOJ investigation? In March 2025, Cal-Maine received a Civil Investigative Demand (CID) from the DOJ regarding alleged anticompetitive conduct and high egg prices, followed by subpoenas from New York and Washington. How much financial and operational distraction will these federal and state probes cause?

• Will the antitrust appeal succeed? In the Egg Products Plaintiffs case, a jury awarded plaintiffs $17.8 million, which was trebled to $43.6 million (for which Cal-Maine is jointly and severally liable). Cal-Maine has posted a $23.9 million bond and is pursuing post-judgment motions and appeals. What is the likelihood of overturning this verdict?

Historic Corporate Governance Shift (The End of Family Control). For its entire history as a public company, Cal-Maine Foods operated as a “controlled company” because the family of late founder Fred R. Adams, Jr. owned all of the company’s Class A common stock, which carried 10 votes per share. However, to facilitate the family’s portfolio diversification, the company executed a massive governance restructuring in April 2025. All Class A shares were converted into standard, one-vote-per-share common stock. Following the conversion and a subsequent secondary stock offering, the founding family’s voting power plummeted from over 53% to roughly 6.1%. To ensure a smooth transition, Adolphus B. Baker (the founder’s son-in-law) agreed to remain as executive Board Chair through at least the 2027 annual meeting.

Bull Case: Scale, Diversification, and Financial Fortress

The bull case is simple: you are buying the dominant, lowest-cost producer in an essential food category at the bottom of its cycle, immediately after the largest governance catalyst in the company’s public history. A ~$3.7 billion market cap less $1.15 billion in cash puts the enterprise value around $2.55 billion for a business that earned over $1.2 billion in a peak year and is structurally raising its trough. The dividend and buyback pay you to wait.

1. Unmatched Scale and a Low-Cost Moat

• Industry dominance: Cal-Maine is the undisputed largest producer and distributor of fresh shell eggs in the U.S., selling approximately 1.3 billion dozen eggs in fiscal 2025—roughly 24% of domestic consumption—with a flock of nearly 50 million layers serving more than 60,000 customer retail locations. That volume reliability makes the company an indispensable supply chain partner to Walmart, H-E-B, and Publix.

• The moat is operational: Vertically integrated “in-line” facilities gather, clean, grade, and package eggs at the location they are laid—eliminating transport costs, reducing labor dependency, and yielding a higher percentage of premium USDA Grade A eggs. The company manufactures the vast majority of its own feed at mills adjacent to its production plants, controlling its largest and most volatile cost. This structure keeps Cal-Maine the low-cost supplier in its markets through every leg of the cycle.

• Scale compounds through M&A: Twenty-six acquisitions integrated since 1989 in a still-fragmented industry, including ISE America (~$110 million, the company’s first production assets in Maryland, New Jersey, and Delaware) and the Mahard Egg Farm turnaround that generated an estimated 260% ROI with a 3.17-year payback.

2. The Transformation Is Showing Up in the Numbers, Not Just the Deck

• The mix shift is real: Specialty eggs grew to roughly 30% to 40% of total sales revenue, driven by consumer demand and state-mandated cage-free legislation, and these volumes price off negotiated, cost-based frameworks rather than the spot market. In Q3 fiscal 2026, specialty shell egg sales ($289.1 million) surpassed conventional ($283.2 million) for the first time, and specialty eggs plus prepared foods combined hit a record 52.9% of net sales. The prepared foods buildout—Echo Lake Foods (waffles, pancakes, frozen omelets), Crepini (egg wraps, protein pancakes), MeadowCreek (hard-cooked eggs), and Creighton Brothers—adds a higher-margin earnings floor, with Echo Lake alone contributing $70.5 million in revenue in its first quarter under Cal-Maine and expected to be mid-single-digit accretive to EPS in fiscal 2026.

• The stress test already happened: Conventional egg prices crashed 70.1% in Q3 fiscal 2026—and the company still earned $1.06 in diluted EPS in a single quarter. In prior down-cycles, entire fiscal years produced $0.38 (FY20), $0.04 (FY21), and a net loss (FY17). The earnings floor has structurally moved, and the hybrid pricing models now applied to conventional volumes raise it further.

3. The Governance Unlock Makes Cal-Maine Acquirable for the First Time

The April 2025 conversion of the family’s super-voting Class A shares collapsed their voting power from over 53% to roughly 6.1%. The controlled-company discount is gone, funds that require single-class voting structures can now own the stock, and—with no controlling family, no debt, and $1.15 billion of cash—the company is exposed to activist campaigns and unsolicited acquisition offers for the first time in its public history. That optionality costs nothing at this price.

4. The Cage-Free Mandate Is a Forced Consolidation Event

Ten states covering roughly 27% of the U.S. population have mandated cage-free egg sales, and the transition costs an estimated $45 per bird—roughly $6 billion industry-wide. Smaller, undercapitalized competitors cannot fund it. Cal-Maine, with zero debt and hundreds of millions already deployed into cage-free capacity organically and through acquisition, is positioned to capture outsized share as the deadlines hit.

5. Capital Returns Pay You to Wait

• Variable dividend: One-third of quarterly net income is reliably distributed to shareholders during profitable periods, giving a current real dividend yield while you hold.

• Active buyback: Management is utilizing the $500 million repurchase program authorized in February 2025, buying back over $100 million in shares in the first three quarters of fiscal 2026. The right of first refusal on the family’s remaining 2.79 million registrable shares—at a 6% discount to the 20-day volume weighted average price (VWAP)—gives the company a mechanism to convert the overhang into accretion.

• The math: Zero long-term debt, $1.15 billion in cash and short-term investments, an undrawn $250 million revolver, and insiders holding a healthy 6.5%. You collect the dividend, the buyback shrinks the float, and the next HPAI supply shock is a free call option you are not paying for.

Bear Case: Financial Cyclicality and Lack of Pricing Power

The bear case is equally simple: Cal-Maine is a price-taker in a brutally cyclical commodity, the trailing numbers flatter the multiple, a third of sales depends on a single customer, and the supply data says the down-leg of the cycle is still building.

1. A Price-Taker in a Glut That Is Still Building

• No pricing power: Cal-Maine does not set prices—most conventional eggs are sold off independent wholesale market quotes like Urner Barry. With the national flock recovering from HPAI, net sales for the first three quarters of fiscal 2026 dropped 25.3% to $2.36 billion, and conventional egg prices fell 70.1% in the third quarter alone.

• Supply is restocking: USDA-reported hen depopulations fell 70.6% year-over-year in Q3 fiscal 2026 and the national layer flock grew 2.2% to 310.8 million hens. The egg cycle’s history is unambiguous: high prices breed flock expansion, expansion breeds oversupply, and oversupply crushes prices for extended periods. The down-leg may be longer and deeper than the entry price assumes.

• Feed is the uncontrollable second variable: Corn and soybean meal represent 53% to 63% of farm production costs, and they swung feed cost per dozen from $0.446 (FY21) to $0.676 (FY23) on weather, war, and logistics. A grain shock landing with eggs at cycle lows squeezes margins from both ends.

2. The “Cheap” Multiple Is a Cyclical Illusion

Fiscal 2025’s $24.95 in diluted EPS was an HPAI windfall, not normalized earnings power. The pre-transformation record speaks for itself: FY18 through FY22 produced $2.60, $1.12, $0.38, $0.04, and $2.72 in diluted EPS, with a loss in FY17. If the structural pivot underdelivers, the stock is priced off earnings the business cannot repeat without another bird flu shock. The bull case requires the transformation thesis to be right; the bear case only requires mean reversion.

3. Walmart Is a Single Point of Failure

Walmart (including Sam’s Club) represented 33.6% of net sales in fiscal 2025 and has run between roughly 29% and 34% for years; the top three customers account for roughly half of total revenue (49.2% in fiscal 2025). Customers generally make no long-term purchase commitments. A consolidated retail base can oppose price increases, dictate cage-free terms, and demand promotional programs—and the loss or material reduction of Walmart volume would be detrimental.

4. Execution Risk in New Verticals

Management concedes its experience operating prepared foods businesses is “much more limited” than in shell eggs, and it now competes against entrenched food manufacturers, restaurants, and grocery chains with decades of category expertise. The Echo Lake remodel has already caused temporary production declines and higher costs, dragging sequential operating margins. Meanwhile, the cage-free buildout—hundreds of millions in capital expenditures against no long-term customer commitments—risks oversupplying a premium product that consumers trade away from in a weak economy, leaving diminished returns on massive invested capital.

5. HPAI Cuts Both Ways

Outbreaks tighten national supply and drive record profits—when they hit someone else’s barns. Outbreaks at Cal-Maine’s own facilities in Kansas, Texas, and Maryland between 2024 and 2026 forced depopulations including approximately 3.1 million layers and 577,000 pullets in 2024 alone, disrupting supply capabilities and forcing millions in biosecurity spend. The “free call option” is only free if the next outbreak isn’t theirs.

6. The Legal Docket and the Family Overhang Are Live

A DOJ Civil Investigative Demand on alleged anticompetitive conduct (March 2025), subpoenas from New York and Washington, and a $43.6 million treble-damages antitrust judgment under appeal create headline, distraction, and settlement risk in a politically charged category. The family still holds 2.79 million registrable shares earmarked for continued sell-down, and the end of controlled-company status invites activist campaigns and unsolicited takeover attempts that could distract management from integrating its acquisitions.

Diversified Chaos · CALM Deep Dive

If this was useful, hit the like button and subscribe — it genuinely helps.

Disclaimer: This report is for informational and analytical purposes only and does not constitute investment advice. All investments involve risk, including the loss of principal. Consult a qualified financial advisor before acting on any information presented here.

AI Transparency: As an AI-integrated publication, this content is synthesized using large language models and generative tools. While these technologies enhance our research workflow, they may occasionally produce inaccuracies or hallucinations. Please use this series for informational and educational purposes only—it is not a substitute for your own due diligence. All images are AI-assisted and provided for illustrative context.

I welcome your feedback and questions in the comments and will respond to as many as possible.

Nice article. This is a stock that would likely be a great buy in a general mkt downturn simply because of their capital structure and I don't see the market for eggs shrinking. Though it could be a good buy now, depending on how aggressive they are with buybacks, keeping a floor on the price.

Do you have a rough estimate of what their run rate free cash flow is on maintenace capex - meaning if they stop acquiring/growing and try to maintain flat revenue going forward? I like to use this metric to get a better valuation of any business.

Either way I plan to look at it in more detail, thanks for the article.